Portfolio Protection Strategies provides a detailed analysis of two different option-based strategies that can be used to protect the value of your portfolio. Each resulting scenario is based on the specific characteristics of your portfolio.

Results for both strategies are presented in absolute (total value) and relative (percentage change) terms. Input parameters and the results outlined below are presented:

- a plot comparing protected portfolio vs unprotected portfolio

- option premium range

- number of options needed for the strategy

- net cost (or profit) of required options

- current value range for the protected portfolio

- final value range for the protected portfolio

Portfolio Protection Strategies was written under the supervision of a highly trained finance professional. Portfolio Protection Strategies is a tool that will give you the insight needed to implement your own protective strategy. Portfolio Protection Strategies is intended for informational and educational use only. Decisions affecting your portfolio should be made in consultation with your financial advisor.

Send Questions or Comments to Apps@SciSyn.com

Look below for screen-shots from the app and a detailed example!

Sample Data Input and Results

Note that all input parameters are defined below. This example shows a portfolio with a value 150,000 dollars that

tracks an index that has a current level of 1250. The correlation of the portfolio with respect to this index is described

by its beta (β is 1.15 in this example). Additional input includes the risk-free rate, volatility of index returns, and

volatility error. Finally, the user enters target down & up percentage limits, and their protective time horizon.

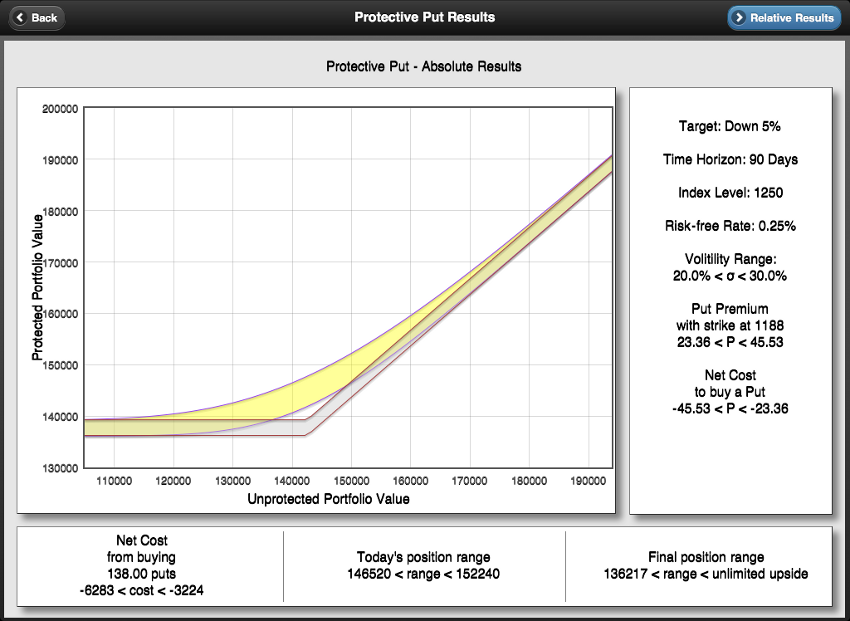

Absolute Results for a Protective Put Strategy are shown below. Relative Results (percentage change) are also available.

The yellow shaded band in the plot shows the current value of the protected portfolio vs value of the unprotected portfolio.

The gray shaded band shows the value of the protected portfolio at expiration vs value of the unprotected portfolio at expiration.

The number of options needed for this protective strategy is 138 put options with a strike price of 1188 (5% lower than current

index level). The cost of taking this position ranges from 3224 dollars to 6283 dollars (depending on the value of volatility).

Accounting for option costs, the portfolio value has a lower limit of 136,217 dollars. This is nearly a 9.2% drop - which is

significantly below our target 5% floor. Main point: costs matter and need to be incorporated into any analysis.

Relative Results for a Protective Collar Strategy are presented below (Absolute Results are also available). A protective

collar strategy requires selling call options and buying put options (at different strike prices). The number of options needed for

this protective strategy is 138 put options with a strike price of 1188 (5% lower than current index level) and 138 call options

with a strike price of 1375 (10% higher than current index level). Taking this position can cost 3.1% of portfolio value or net

a profit of 0.7% of portfolio value. Under ideal circumstances it is possible for premiums received from selling call options to

cover the cost of buying the required put options. Accounting for option costs (or profits), the portfolio value at expiration

ranges from a drop of 8.1% to an increase of 10.7%. Note that this more realistic analysis (including a range of option costs)

differs significantly from our target range of 5% down to 10% up. Option costs extend the downside, and upside, ranges.

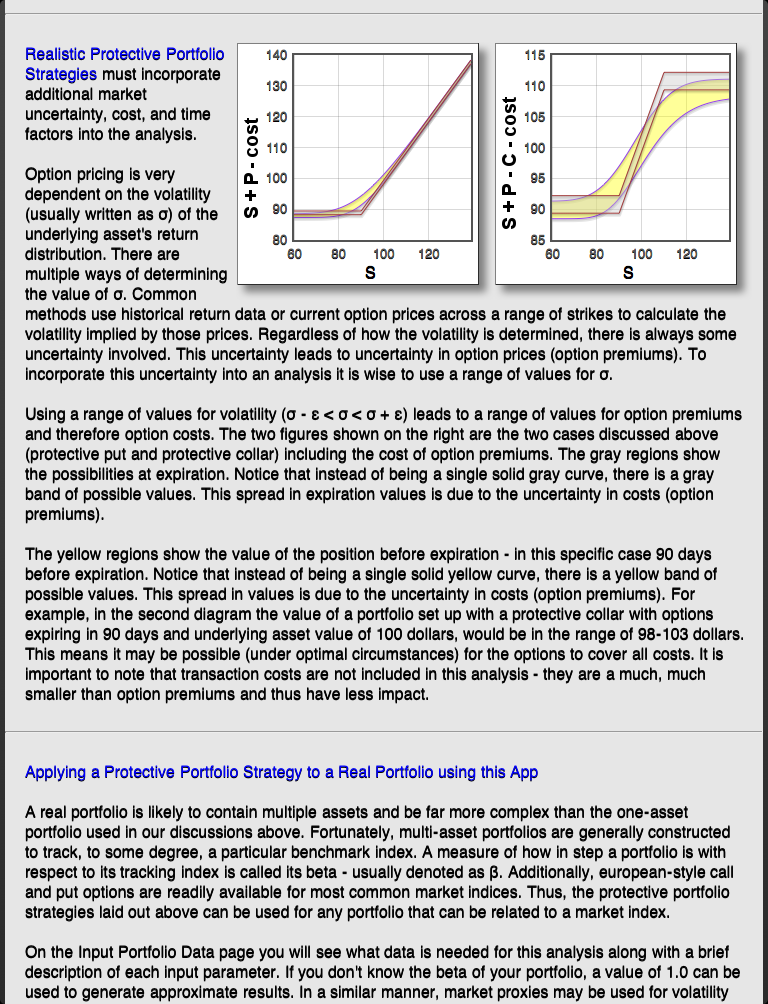

A screen-shot of part of the included Background Information is shown below.

The concepts needed to understand how to apply protective strategies is presented in detail.